About Us

Vaughan has 26 years of experience as an analyst, with the last 13 years spent in Institutional Asset Management Macro research and Portfolio management.

Vaughan Henkel , BSc(Elec. Eng), CFA, CAIA

Vaughan has 26 years of experience as an analyst, with the last 13 years spent in Macro research and Portfolio management. His Portfolio management skills include Multi-Asset (incl. Equity, Bonds and others), Equity both local and Global, Absolute return investing and Hedge Funds.

He has managed numerous teams of analysts in both global and local investment businesses.

His last corporate position was at PSG Wealth, where he provided Portfolio guidance and research to the Advisor network on Local and Global equities and SA Property.

His style is Macro-Fundamental-Quantitative in order to capture returns for clients where they may be found and at his core strives for Pragmatic and Asymmetric outcomes.

The Cyclist Investments Philosophy: More Than a Name, a Mindset

The name “Cyclist Investments” was chosen with deep intention. It perfectly encapsulates the fundamental reality of financial markets: their inherent cyclical nature.

Just as a cyclist understands that discipline, training, analysis of data, practice and endurance is required to ready oneself for every hill climb ascent. Similarly, skills such discernment, pacing and measure are required for any descent.

The Cyclist Investments team knows that periods of market strength and weakness are inevitable. These cycles are driven by the timeless human pendulum swinging between unchecked optimism and undue pessimism. Our philosophy is built not to fear these cycles, but to navigate them with discipline and foresight.

The Investment Journey, Framed by Cycling

For our founder, a keen and seasoned road cyclist, the analogy is perfect. The journey of investing mirrors the experience of a long-distance ride:

Hills & Headwinds

Represent market downturns and economic challenges. We prepare for them, shift gears, and persevere, knowing they are temporary.

Descents & Tailwinds

Symbolize periods of positive performance. We maintain control and discipline, avoiding complacency when the riding is easy.

Rain & Shine

The variable conditions of the global economy. We are equipped for all seasons with a robust, adaptable strategy.

The Peloton

Illustrates market herd behaviour. While there is safety in the pack, true outperformance often requires the courage to break away when the opportunity is right.

Crashes & Winds

The inevitable setbacks and successes. We learn from both, building resilience and refining our process for the long tour ahead.

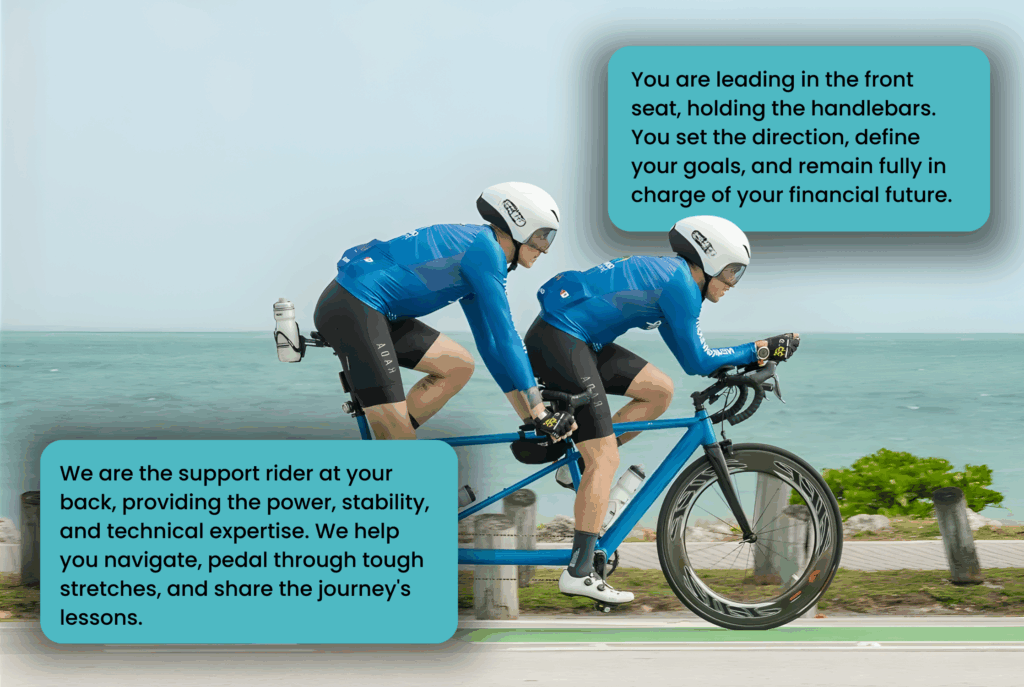

Why investing is like cycling

On a tandem bicycle, success depends on perfect partnership. In our model:

We are the support rider at your back, providing the power, stability, and technical expertise. We help you navigate, pedal through tough stretches, and share the journey's lessons.

You are leading in the front seat, holding the handlebars. You set the direction, define your goals, and remain fully in charge of your financial future.

We succeed only when you do. This symbiotic partnership ensures that our expertise is directly channeled towards your objectives, creating a unified path to long-term wealth creation. Together, we ride the markets’ cycles, prepared for every hill and headwind, and poised to capitalize on every stretch of open road.

Pragmatic & Asymmetric

Our approach

Our investment approach is built on a foundation of pragmatism, seeking to balance economic and market cycles with disciplined security analysis. We balance growth while being valuation-sensitive, thereby avoiding overpriced hype.

Our goal is to identify opportunities with asymmetric risk-reward – where the potential upside significantly outweighs the potential loss.

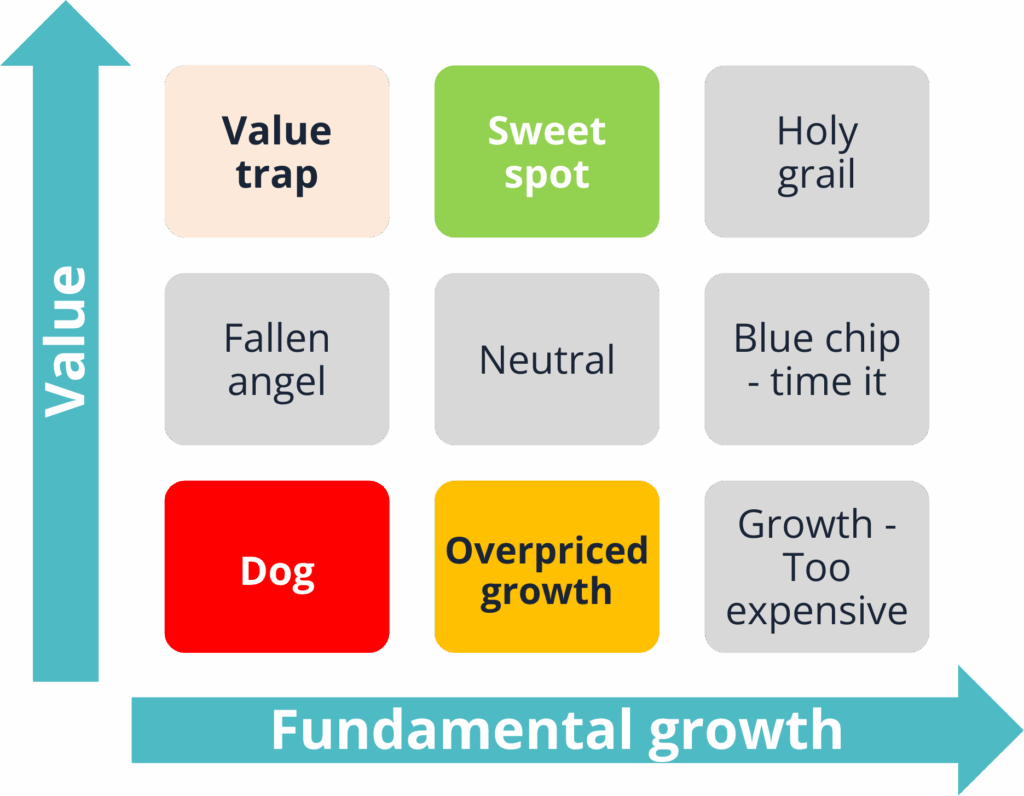

We categorise potential investments to avoid common pitfalls and focus our capital:

The Sweet Spot

Our primary target. Companies with fundamental growth, high and consistent returns on equity (ROE), and a clear catalyst.

Overpriced "Growth"

To be disciplined against. These are often high-quality businesses but are priced for perfection, leaving no margin of safety.

Value Traps

To be avoided. These are statistically cheap companies without a durable competitive advantage or growth pathway.

Dogs

To be avoided. These are statistically cheap companies without a durable competitive advantage or growth pathway.

- Value Traps and Dogs: To be avoided. These are statistically cheap companies without a durable competitive advantage or growth pathway.

- Overpriced ‘Growth’: To be disciplined against. These are often high-quality businesses but are priced for perfection, leaving no margin of safety.

- The Sweet Spot: Our primary target. Companies with fundamental growth, high and consistent returns on equity (ROE), and a clear catalyst.

A Disciplined, Two-Step Framework

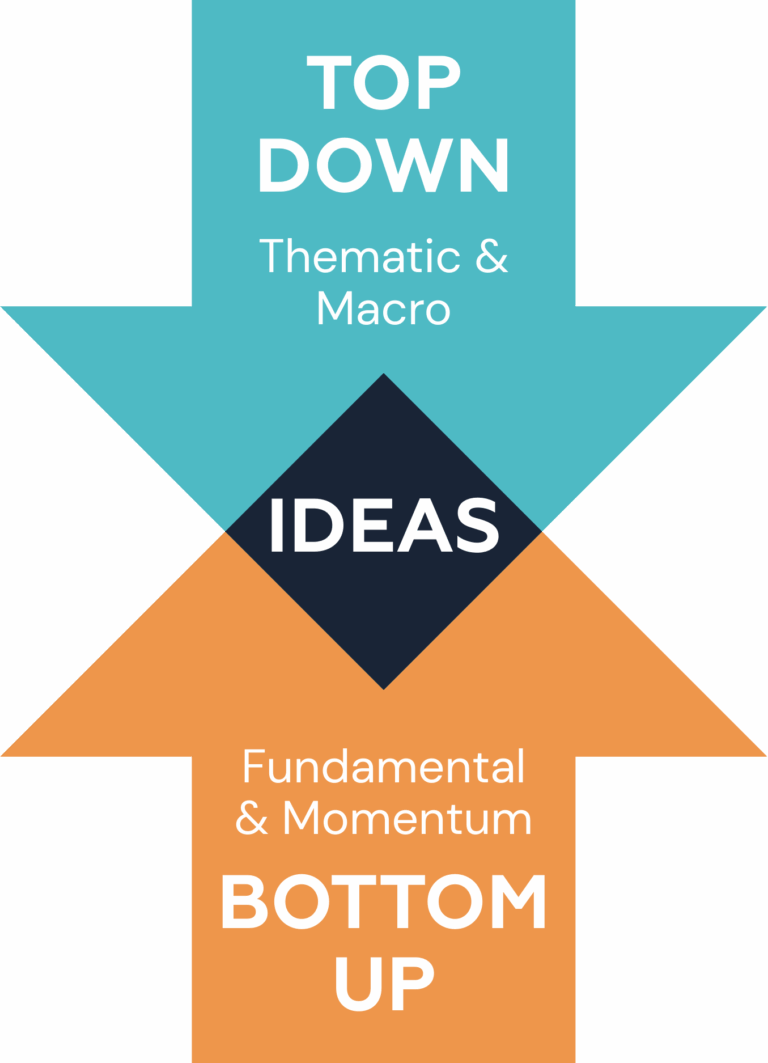

1. Sourcing & Thematic Screening

We generate ideas from a dual perspective:

- Top-Down (Thematic & Macro): We start with a high-level review of the economic and macro landscape to identify powerful, long-term thematic tailwinds.

- Bottom-Up (Fundamental & Momentum): We simultaneously screen for companies exhibiting strong fundamental qualities (e.g., Moats, superior Management , high ROE, consistent earnings) and positive price momentum.

2. The "10th Man" Deep Dive & Position Structuring

This is our core analytical and risk-management engine:

- Fundamental Diligence: Every idea must possess a simple business model, high-quality fundamentals (High/Consistent ROE, Limited Leverage), and operate in a favorable environment (Limited Regulation, Limited Disruption).

- The “10th Man” Review: To combat groupthink and confirmation bias, we formally adopt a contrarian “10th Man” role. This process mandates a dedicated effort to challenge the thesis, actively seeking disconfirming evidence and opposing viewpoints.

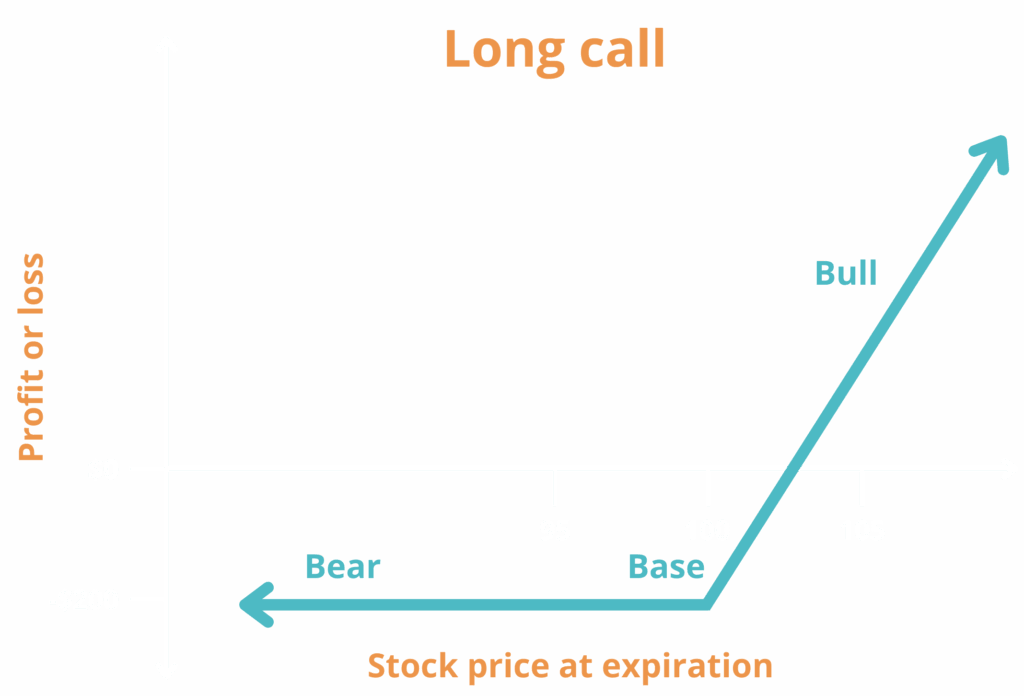

- Asymmetric Position Structuring: We use option-type thinking, to define and limit our risk. This creates a pre-determined, worst-case loss profile (e.g., the premium paid), while preserving unlimited upside, perfectly aligning with our asymmetric philosophy. Our profit/loss is not linear; it is designed to have a capped loss and uncapped gain.

The core of strategic investing is the recognition that superior returns are ‘lumpy’ and non-linear. They come from a small number of asymmetric bets where the upside vastly exceeds the risk. Any process that prioritizes the elimination of risk, inherently sacrifices these exceptional outcomes, settling instead for consistent but mediocre returns.”

“In 58 years of Berkshire management, most of my capital allocation decisions have been no better than so-so. Our satisfactory results have been the product of about a dozen truly good decisions – that would be about one every five years.”

– Warren Buffett, 2022 letter to Shareholders.